Reducing Debt: A Comprehensive Guide to Debt Management

Home » Blog » Personal Finance » Reducing Debt: A Comprehensive Guide to Debt Management

In today’s financial landscape, managing debt has become an integral part of achieving and maintaining financial stability. Whether it’s credit card balances, student loans or personal loans, a strategic approach to debt management can make a significant difference in your financial well-being. In this guide, we’ll explore key aspects of effective debt management, including understanding credit scores, prioritising high-interest debts, the compounding effect of interest, consolidation and refinancing, as well as the benefits and risks of the “pay later” phenomenon.

Understanding Your Credit Score

Your credit score is a numerical representation of your creditworthiness. It plays a crucial role in determining the interest rates you’ll be offered on loans and credit cards. A higher credit score generally leads to better terms and more favourable financial opportunities. Regularly monitor your credit report and score, and take steps to improve it by paying bills on time, reducing credit card balances, and managing debts responsibly.

Prioritising High-Interest Debts

When dealing with multiple debts, it’s important to prioritise those with the highest interest rates. High-interest debts can quickly snowball, making them more challenging to pay off over time. By tackling these debts first, you minimise the overall interest you’ll pay and expedite your journey toward becoming debt-free.

The Compounding Effect of Debt Interest

The concept of compound interest applies not only to savings but also to debt. The longer you carry a debt balance, the more interest accumulates, and the greater the financial burden becomes. This underscores the importance of prompt debt repayment to minimise the compounding effect and regain control of your financial situation.

Consolidation and Refinancing

Debt consolidation involves combining multiple debts into a single loan, often with a lower interest rate. This can simplify your monthly payments and potentially reduce your overall interest costs. Refinancing, on the other hand, entails replacing an existing loan with a new one that offers more favourable terms. Both strategies can provide relief and streamline your debt management efforts.

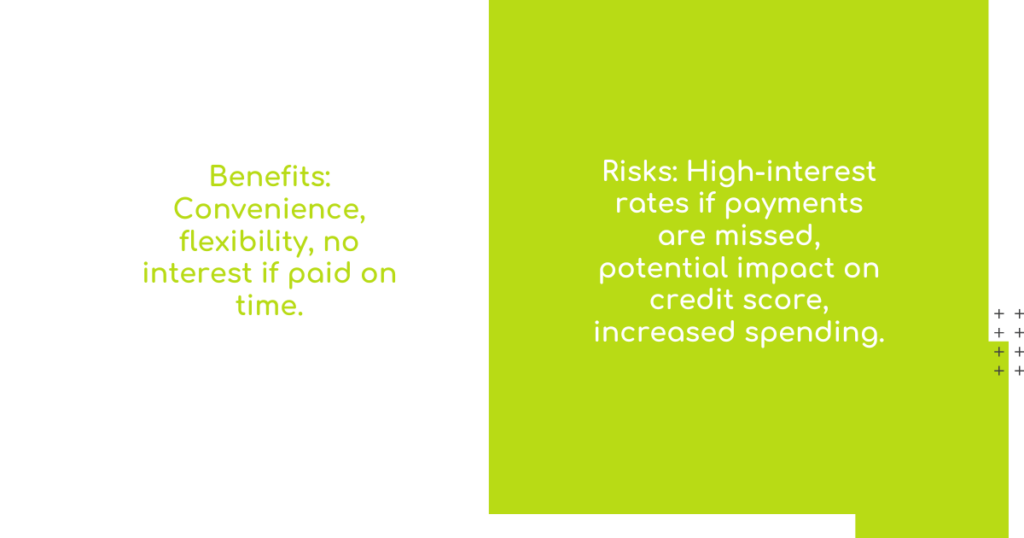

Benefits and Risks of “Pay Later”

The deferred payment phenomenon, popularised by services like Buy Now, Pay Later (BNPL), offers convenience and flexibility in making purchases. While it can provide short-term relief, it’s essential to consider the long-term implications. These services often come with interest or fees if payments are not made on time. Before utilising “pay later” options, assess your ability to meet the payment deadlines and understand the potential impact on your budget and financial goals.

Crafting Your Debt Management Strategy

Assessment: Begin by taking stock of your debts, interest rates, and repayment terms.

Relevant

- Budgeting: Create a comprehensive budget that allocates funds for debt repayment while covering essential expenses.

- High-Interest Debt First: Prioritise paying off high-interest debts aggressively to minimise interest costs.

- Consolidation and Refinancing: Explore consolidation and refinancing options to streamline payments and potentially reduce interest.

- Credit Score Maintenance: Consistently work on improving your credit score through responsible financial behaviour.

- “Pay Later” Evaluation: Exercise caution when using “pay later” services, ensuring they align with your financial capacity.

Debt management is a journey that requires diligence, discipline and informed decision-making. By understanding your credit score, prioritising high-interest debts, being aware of the compounding effect of interest, exploring consolidation and refinancing, and carefully evaluating “pay later” options, you can navigate the complexities of debt with confidence.

The path to financial freedom is achievable with a strategic approach to debt management and a commitment to regaining control of your financial future. Speak to an advisor at Financial Life Design and take charge of managing your debt.

Related Posts

Nurturing Tomorrow’s Minds: How to Plan for Your Children’s Education – A Guide for Expat Families

As parents, providing a sound education is one of the most valuable gifts we can give our children.

Safeguarding Your Wealth: The Essence of Asset Protection

Asset protection is a cornerstone of financial security and peace of mind. It involves identi

Business Travel: Company Insurance, MNCs, SMEs and Global Destinations

In the dynamic landscape of modern business, the world becomes a canvas upon which opportunities are